Human HD(TYO.2415)

Almost Net-Net, PER<7x, Negative EV, Dividend=4%, Upward Sales/Profit Growth in staffing service amid labor shortage in Japan.

Summary

Business : Staffing Service, Education, Senior Care

Valuation : Almost Net-Net, PER=6.7x, Negative EV

Dividend: 64 yen (FY2025 forecast), expected dividend yield = 4.2%, expected payout ratio = 30%

Future Catalyst : Growth in ‘Human Resource‘ segment, Diviende Increase, Share Buy backs.

Risk : AI Substitution, Competition to gather staff candidates

My Position: Holding (average buy price = 1,054 yen)

Business Analysis

Understand at a glance

What does Human HD do?

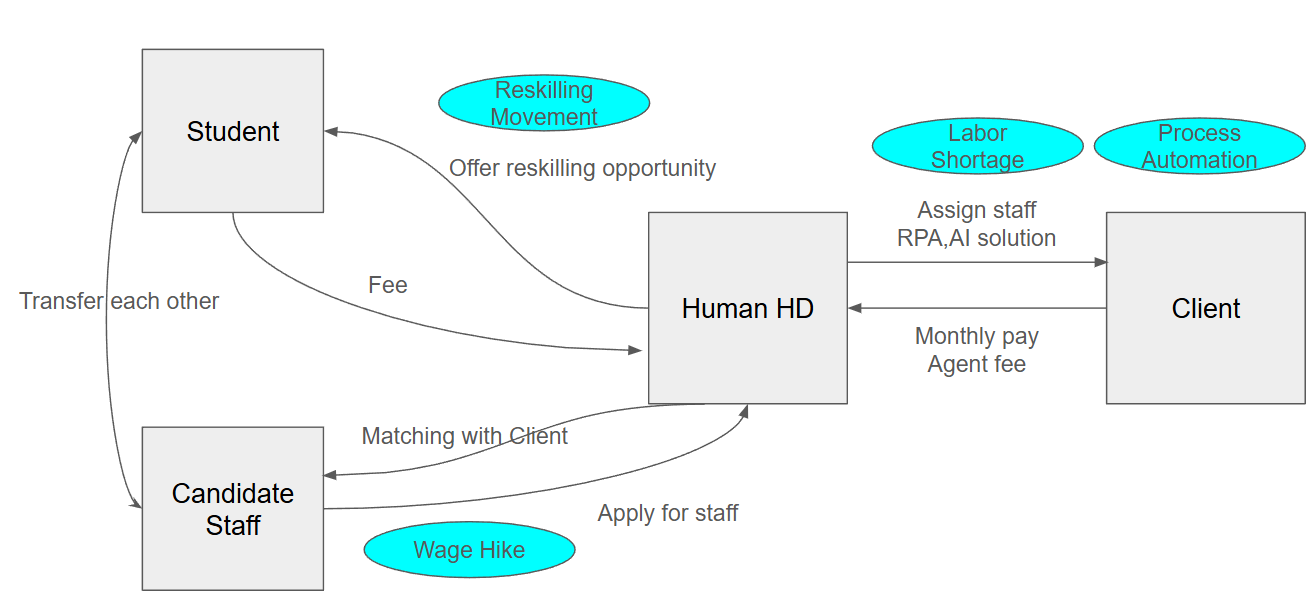

Human HD business can be divided to ‘Human Resource’, ‘Education‘, ‘Senior Care‘. They make money mainly from ‘Human Resource‘ segment. In this segment, they assign a staff to clients which monthly pay to Human HD. When a saff is employed in clients, Human HD receives agent’s fee for introducing a staff. The job types are various including ‘Office work‘, ‘Creative Design‘, ‘Sales‘, ‘Engineer‘, ‘hospital work‘ etc…

Also, not only for introducing human resources, Human HD offers the solution for client’s business process issues by RPA(Robotic Process Automation).

In the ‘Education‘ segment, Human HD offers the opportunity to learn business, technical skills for adults who want a reskilling.

*The other segments are less important, skip the details.

Business Performance & Competitive Environment

Both sales and profits are increasing. Japan is facing a labor shortage due to a declining population. The population problem cannot be easily solved, and this situation will continue for a long time. Because there is a shortage of people, clients have a high demand for human resources & business process automation, which is a tailwind for ‘Human Resource‘ business.

Moreover, as the traditional lifetime employment system becomes outdated, the term "reskilling" is becoming more and more commonly heard in Japan, so the external environment surrounding the ‘Education‘ business is also favorable.

*Gray line is sales.(10 years CAGR = 4.72%)

*Red line is operating profit.(10 years CAGR = 4.81%)

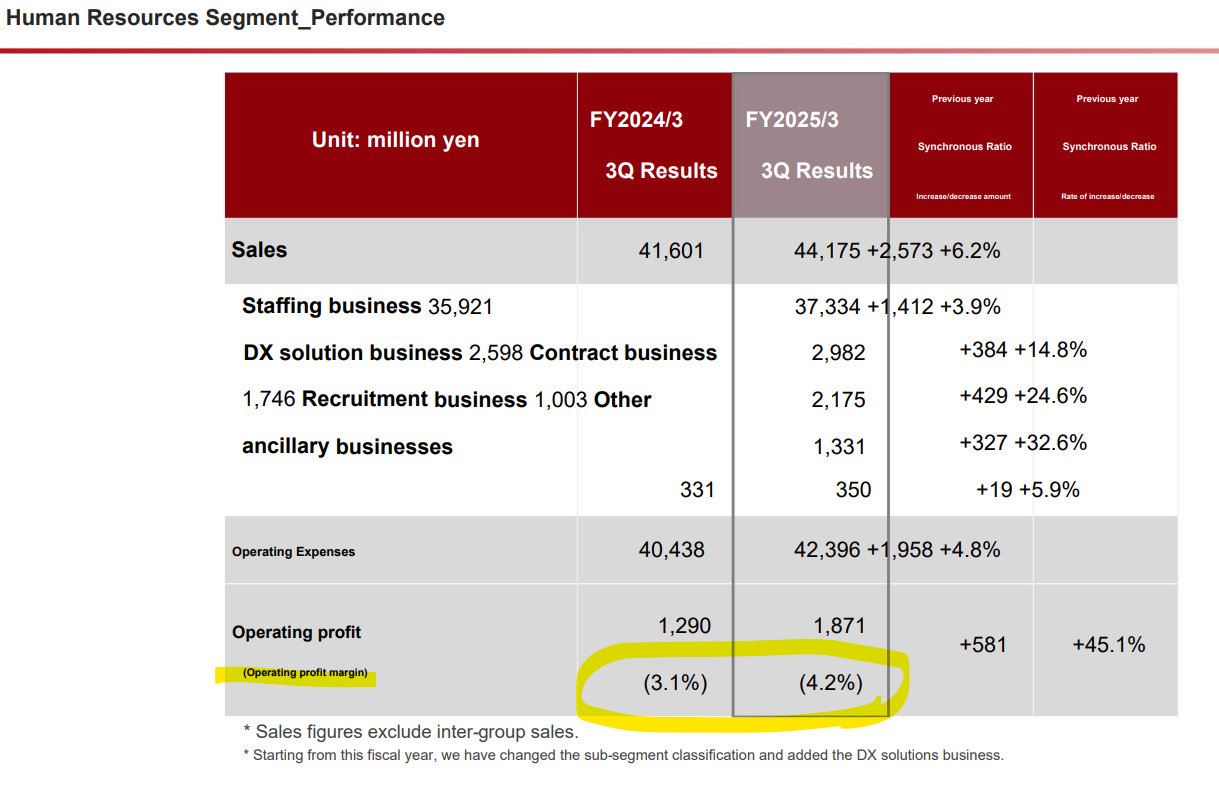

According to the latest earning result, both growth of sales/operating was realized, especially in ‘Human Resource‘ business based on the high demand of staffing as mention above.

*’人材’ is ‘Human Resource‘ segment.

Next, look into supply side. Offering the staff to clients, Human HD needs to attract candidates at first. They can obtain it from ‘Education‘ business. Assigning the new job process is included in at the end of Education Program, so students are transferred to staff candidates smoothly. Also, there exists a reverse flow(candidate staff → student), Human HD offer reskilling program to them. It means ‘Human Resource‘ and ‘Education‘ business have synergies.

Basically, candidates are not high-end class, so it’s difficult for them to promote effectively to clients themselves. They need a support for client-candidate matching, how to self promotion and after care service etc... Because Human HD is a listed company and has a sufficient sales/customer service function, candidate staffs feel a good.

Looking at the breakdown of sales, general and administrative expenses, advertising expenses have decreased. This is good as Human HD are able to approach candidate staffs and clients efficiently. The external environment looks favorable at both the demand and supply sides.

In terms of relationships with suppliers, note the current wage environment. In Japan, wages did not rise for a long time, but due to inflationary conditions, wages are now showing an upward trend. (*In Japan, the period since the 1990s, when wages did not rise, is referred to as the ‘lost decades’.) As the cost of gathering candidate staffs is rising, Human HD are negotiating with clients to increase unit prices. Judging from the improvement in operating profit margins, it appears that price pass-through is working well.

Risk : AI Substitution threat or New opportunity?

The job types offered by Human HD are not highly skilled, so as AI continues to evolve and be introduced, there is a risk that these people will be replaced. I don't think that's going to happen anytime soon, but we need to keep a close eye on the situation. On the other hand, there will likely be the new demand for support in introducing AI to clients. They have started offering the AI introducing support. Given the knowledge of client business process issues, I expect they will capture the AI-related demand which improves the Price/Mix of Human HD. (*In fact, they have been capturing demand for RPA(Robotic Process Automation) following a similar approach.)

Valuation

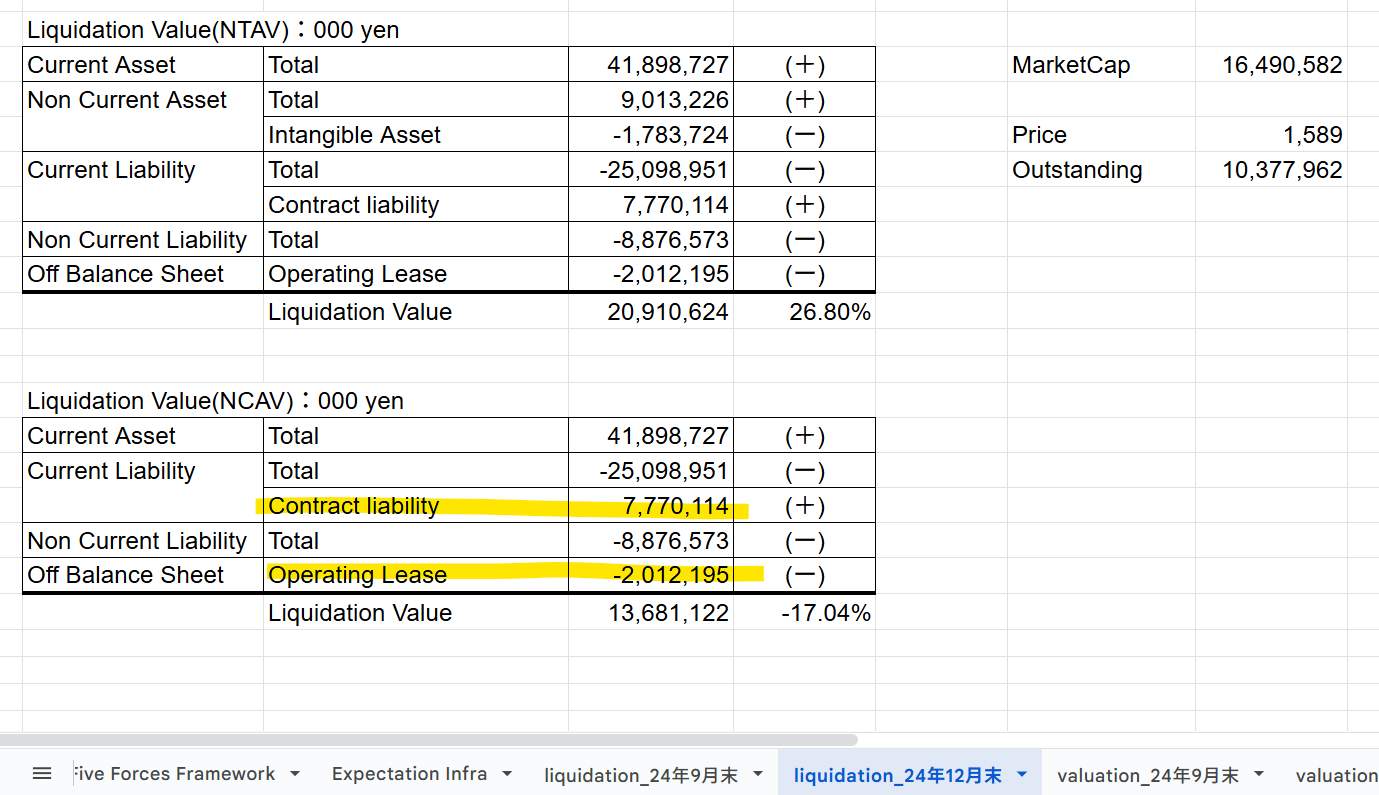

Based on the latest financial position in FY2025 Q3, it’s almost Net-Net stock.

Just to add a supplement. First, it’s for ‘Contract liability‘. When calculating NCAV, all liabilities are removed (-), but in this case, Contact Liability (+) was not removed. ‘Contract liability’ is mainly admission fees and tuition fees in the education business. These payments from students are recognized as revenue in sequence, so the portion that has not yet been recognized as revenue is a contract liability.

The admission fee included in the contract liability is non-refundable, so it has been adjusted when calculating the ‘Liquidation Value’.

Second, it’s for ‘Operating Lease‘. This does not appear on the balance sheet, but it is essentially treated as a liability, so I remove it like any other liability when calculating the liquidation value. I assumed this is for school buildings used in the education business under lease agreements. Since the contracts cannot be cancelled, even if the company goes into liquidation now, the payment will still be required. It’s liability characteristics.

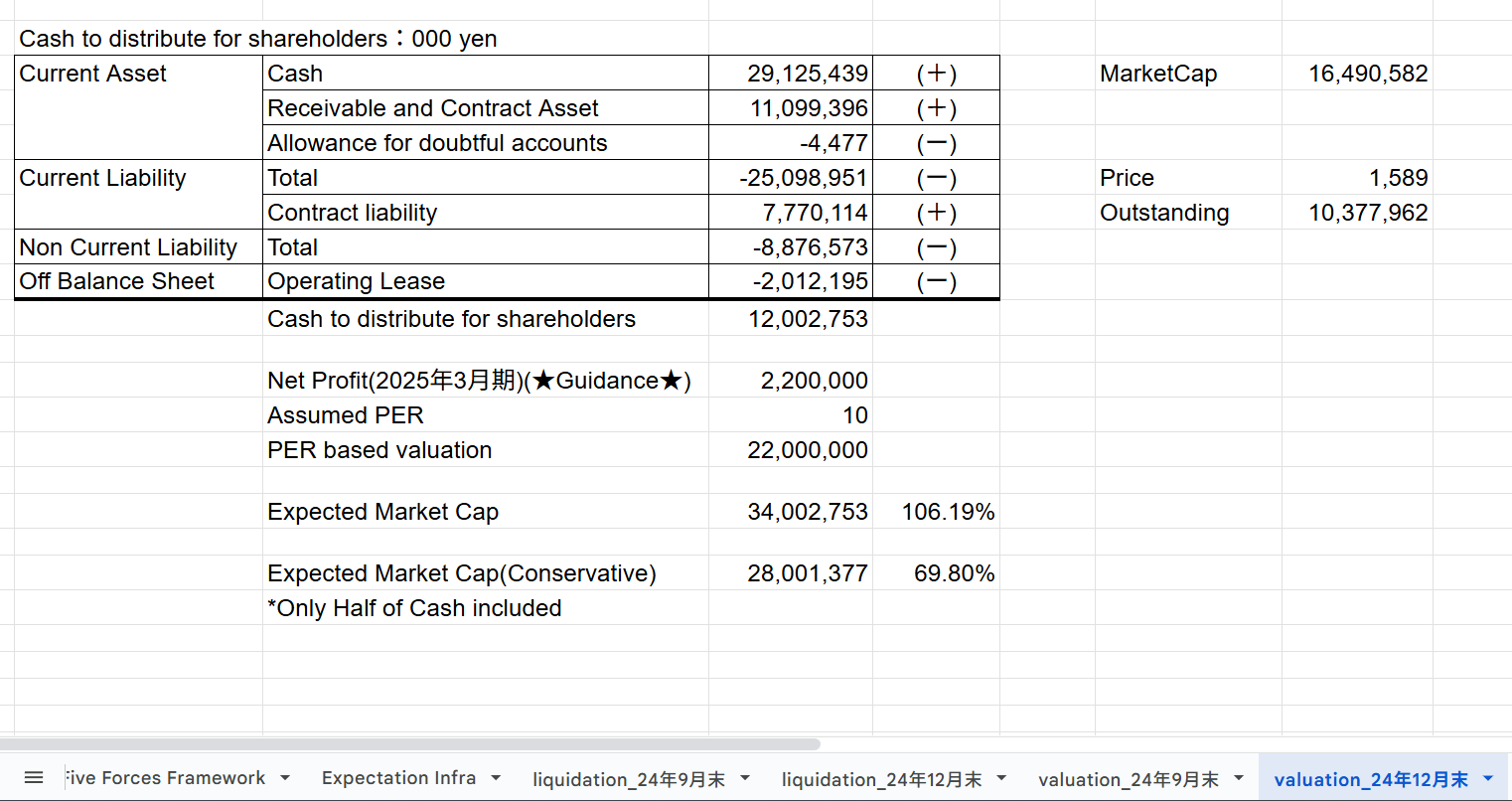

Looking at Human HD's asset structure, it has a large amount of cash, with cash + accounts receivable accounting for 95% of its current assets.

Due to huge amount cash, “Cash to distribute for shareholders“ + PER valuation has the upside 69%~106%. Current PER<7x, but I believe that assumed PER = 10x is still conservative, considering the solid sales/profit growth.

Furthermore, Human HD’s Enterprise Value is the negative which shows that they have an abundant cash.

*’企業価値’ is Enterprise Value.

Shareholder Return

So, will the abundant cash be returned to shareholders? Last year, the company significantly increased its dividend, and expected dividend is 64 yen in FY2025, with a dividend yield of 4.2%.

The dividend policy has been changed, and the target dividend payout ratio has been increased from 20% to 30%. The company bought backs. (※4.55% of the total number of issued shares) From the perspective of shareholder returns, it's not bad.

Conclusion

Japan is experiencing a shrinking domestic demand due to a declining birthrate, aging population. Human HD is benefiting from the chronic problem of labor shortages in this external environment. CAGR of sales is 4.7% over the past 10 years, and I think it is possible for it to continue to grow in the future. If so, the current PER<7x is too cheap. Also, they have plenty of cash and try to distribute them to shareholders. Dividend yields over 4% is not bad. Human HD is “Growh/Value/High Dividend” stock. The stock has risen by over 50% since I bought it, but I still believe it is undervalued.

Earning Update

After this article published, I added to earning update. Please refer as follow.

Great to see you on substack. I used to follow you on note.com with a translator app. Out of curiosity, are there other investors on note.com you think post good ideas?