Noda(7879)

Price revision will improve the margin, Net-Net, Dividend 5%, Normalized PER is 5x(?), Turnaround will be soon?

Hello. In my substack, I share the stock analysis in Japanese market, especially Net-Net Stock. If you enjoy my article, you can subscribe & share to your friends. Thank you.

Summary

I will share the stock analysis for Noda(7879), which is a wood materials marker for residential buildings. At first, for disclosure, I have a small long position in this stock.

The current stock price was down 50% from at the high price in 2023. This is because the profit was significantly declined due to the fall in price of Noda products. Their products are used in a single-family home, but there is a slowdown in housing starts due to the construction price hike(material price, human resource shortage etc..) and interest rate hike. On the other hand, after COVID-19, the each marker produced wood materials, which increased the inventory. Weak demand and excess inventory cause the price down…

Because marker started the production control, the over production was ending and price was stabilized.

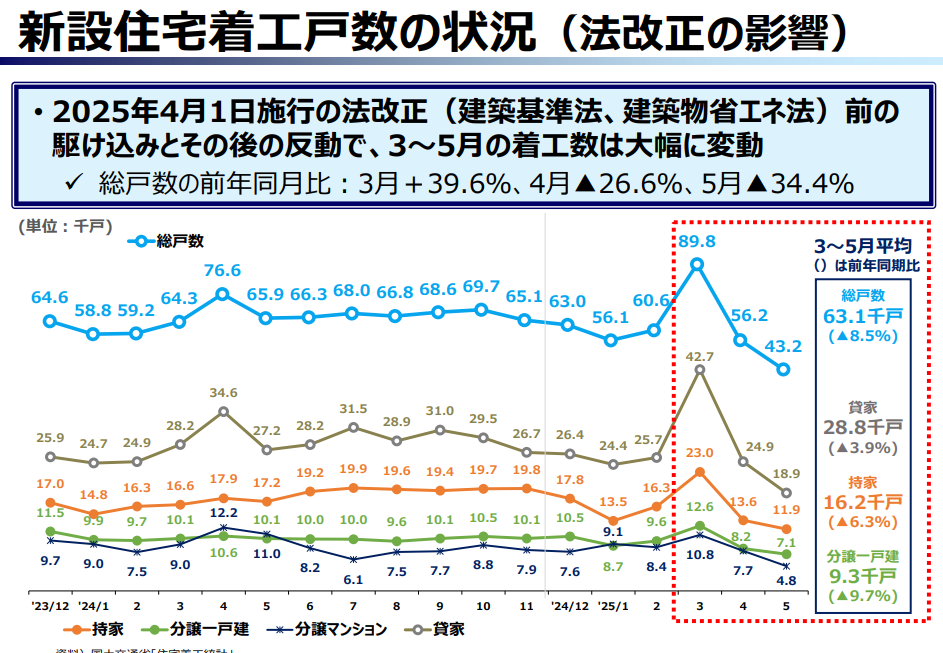

Although the housing starts decreased significantly in April, May in 2025 due to the plunge following the last-minute spike in demand for an amendment to the Building Standards Act. However, according to the latest statistics, the housing starts get better, which Noda can pass on the cost to price in the near future. Margin will be improved.

Of course, Japan faces the population decline, so the housing starts for a single-family home increasing will not be expected. Thus, Noda tries to strengthen the rental housing market and non-residential market. In fact, the sales increased YoY in the latest earning result FY2025 Q2 by getting the business opportunity of except for a single-family home.

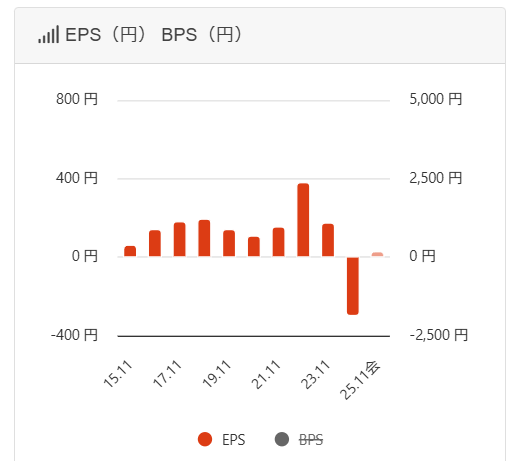

Current PER is 28x based on the FY2025 guidance. However, if the turnaround is succeed mentioned above, then EPS will back to FY2023 level, PER will be 5x. This is the cyclical play.

Finally Dividend. Current yield is 5%. Although the expected payout ratio is over 100% in FY2025, considering the Noda is Net-Net and net debt(=debt-cash) is negative(-9,940 million yen : cf. Noda market cap is 11,300 million yen), I believe the dividend payment is safe. Also, divided will increase more after turnaround. Again, current yield is 5% even if the business situation is tough now. It’s good enough for me.

Business Backgroud

Understanding at a glance

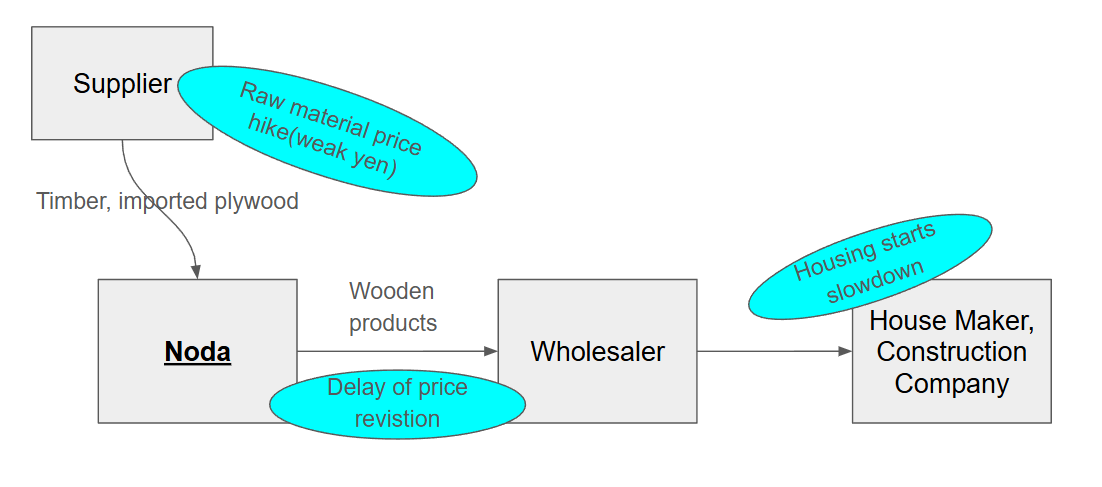

Noda has two business segments.

Wood Materials Business

They produce the interior building materials for floor, door, stairs, etc..

Their products are mainly used in residential buildings. But, Noda tries to expand the business filed to non-residential one(ex. nursing home, kindergarten, exterior construction)

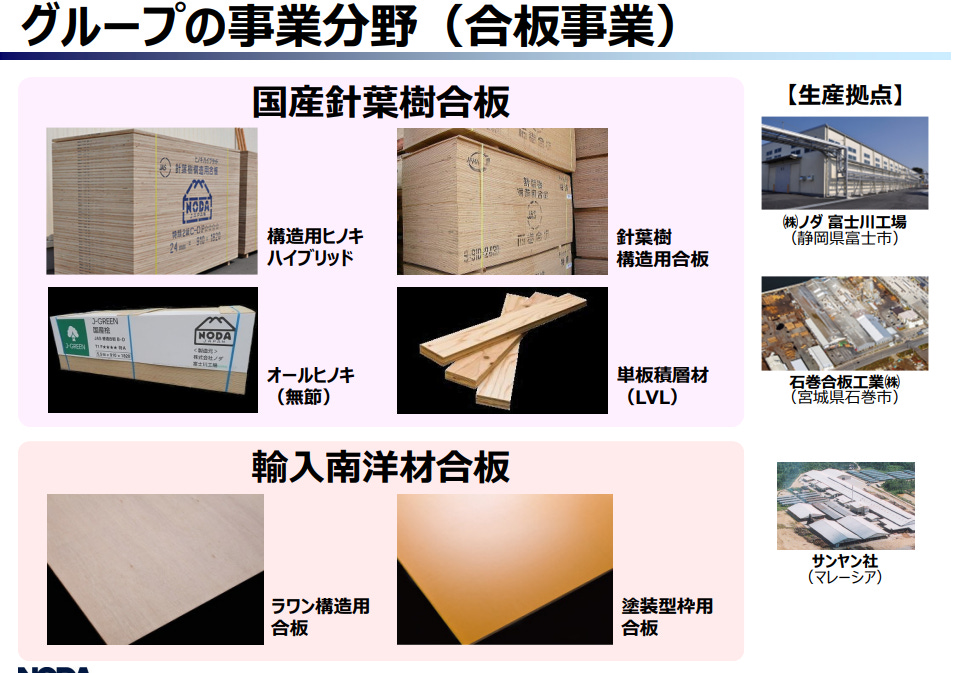

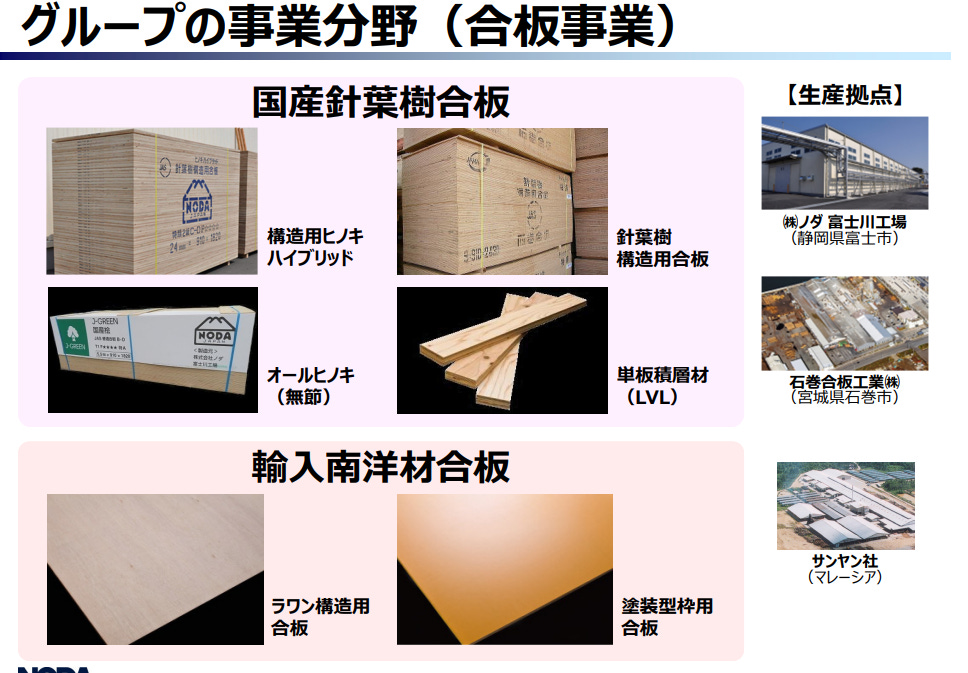

Plywood Business

Noda plywood is produced by Japanese wood in Shizuoka Prefecture. Also, they handle imported wood. Due to the weak yen, imported wood cost increases, which has a negative impact on margin.

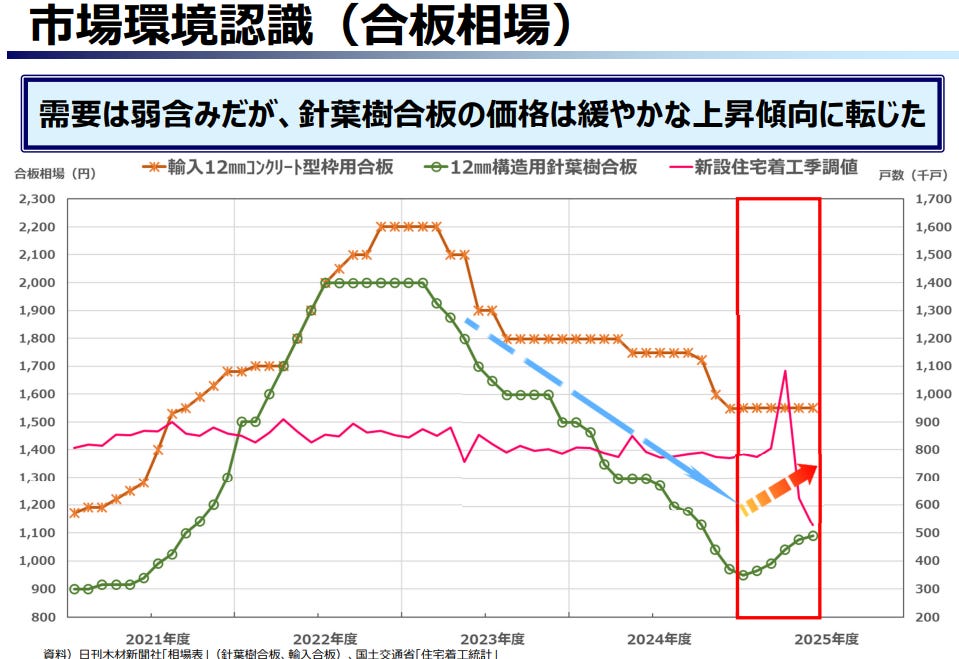

Plywood price has declined from 2023 due to the oversupply and weak demand for a housing starts. This is the reason why plywood segment profit decrease significantly. However, the price has just turned around little recently.

My Investment Thesis

Noda stock price declined over 50%. Why?

The stock price was down 50% from at the high price in 2023. According to the financial info, the profit decreased significantly in FY2024, where the impairment loss was included after re-evaluating non-current asset based on the tough business environment.

The main reason for this difficulty is an imbalance between the demand/supply for a wood material. For demand side, the housing starts especially for a single-family home is a slowdown, because the total cost increases recently due to the land, raw material, human resource cost up and interest rate hike. Family home is a relatively low asset value compared with a condominium in Japan. So. Family home demand is more price sensitive.

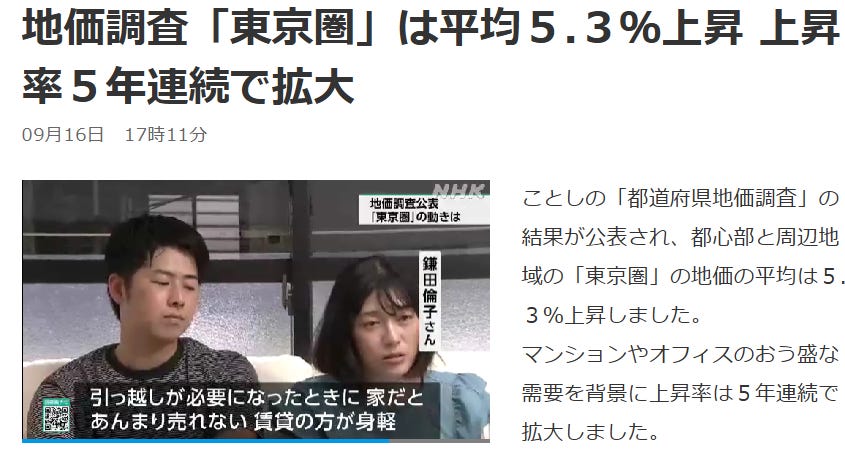

*This new is reporting the land price around Tokyo is up for five consecutive years. Some people tend to select renting a home, not owning.(Link)

Based on such situation, the housing starts data shows the single family home demand is weak(*note rental home is relatively solid). Most of all single family home is wooden, so this weak demand has a negative impact on Noda. (Link)

Next is supply side. After COVID-19, the demand was strong, but from 2022, over supply cause excess inventory. This is the reason why the Noda product price has dropped, which deteriorated margin.

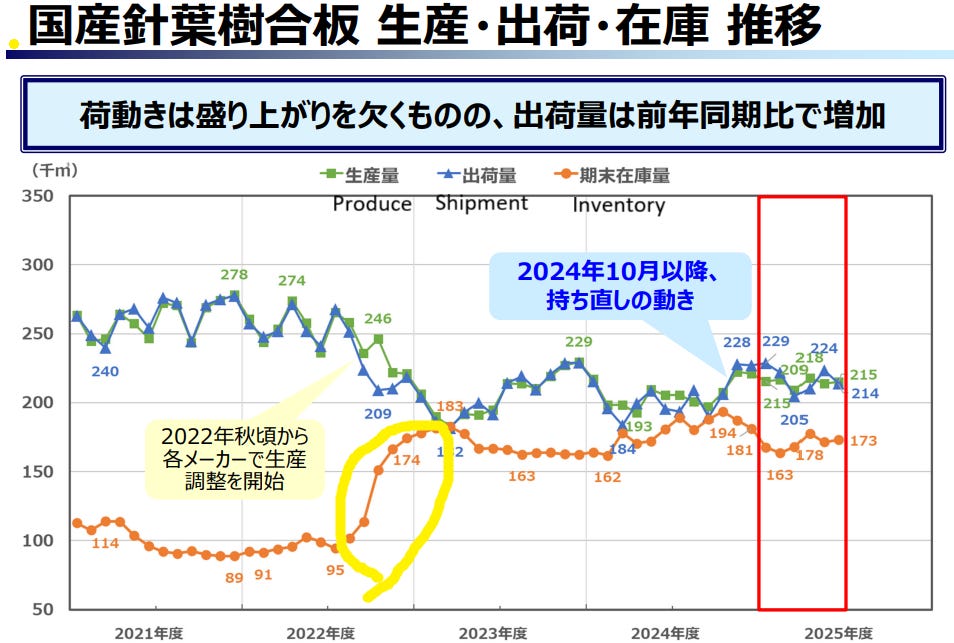

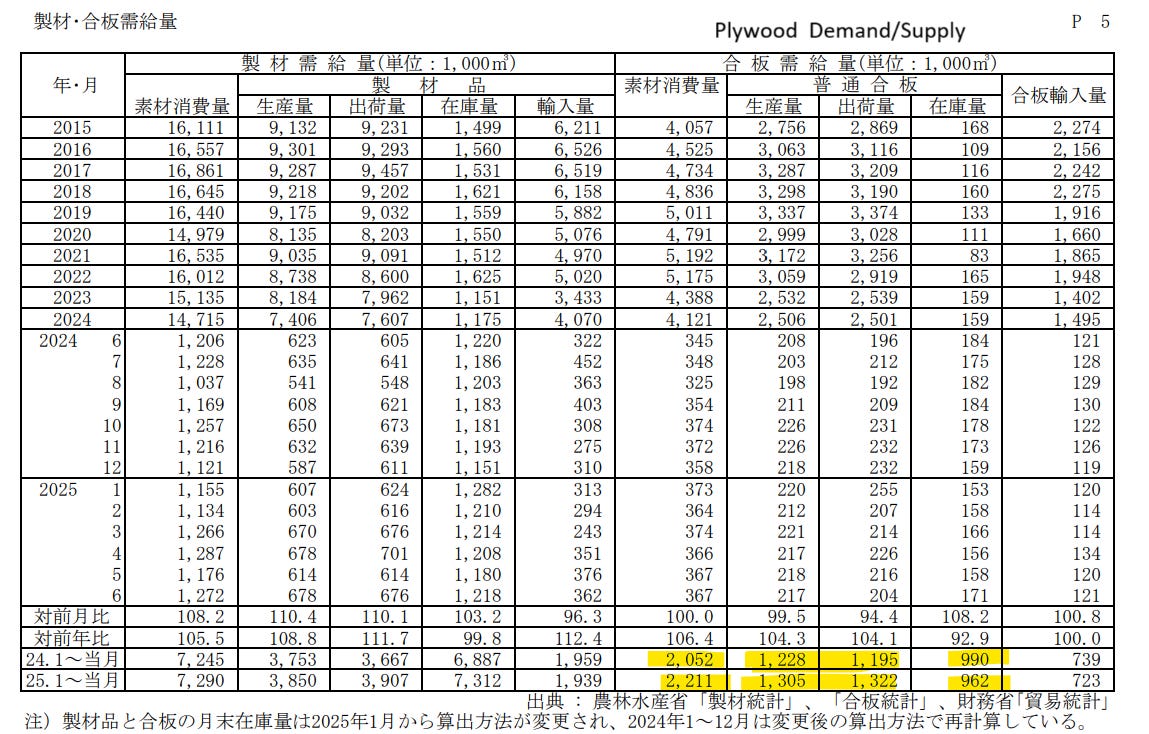

Oversupply is over. Noda gets ready for rationalizing product price.

Wood marker has started production control from late 2022. According to the latest data, Production(生産量) < Shipment(出荷量) in 2025, Inventory(在庫量) decreases, Cosumption(素材消費量) increases. Of course, the situation doesn’t recover greatly, but I can see a sign of a turnaround.(Link)

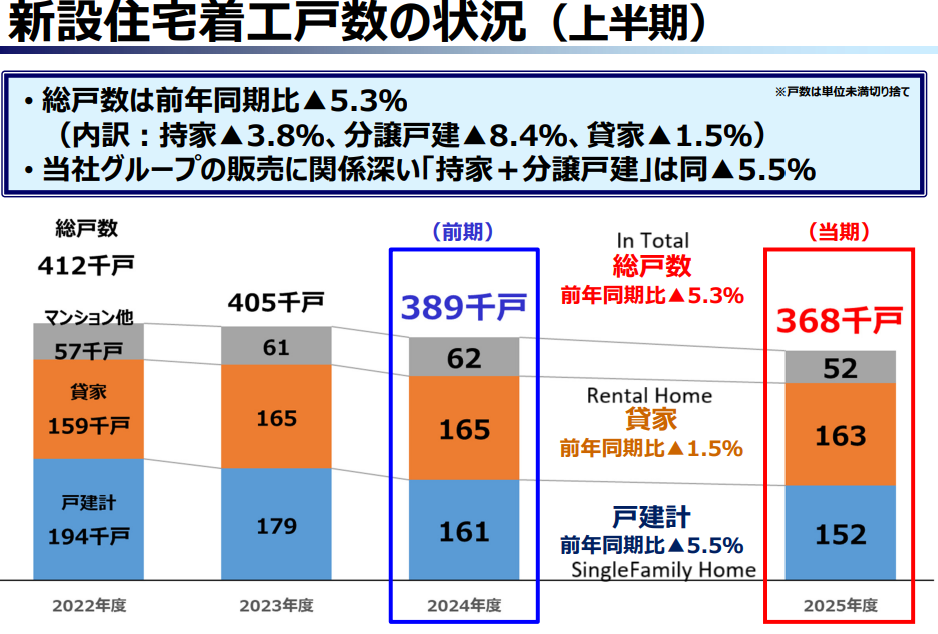

With regard to demand side, one note for the housing starts data, you find the number declined significantly in April, May 2025. This is because the plunge following the last-minute spike in March 2025. The amendment to the Building Standards Act enforcing from April in 2025 requires more eco-friendly specification. This change brings the cost up, so home builders tended to start in a hurry in March in 2025.

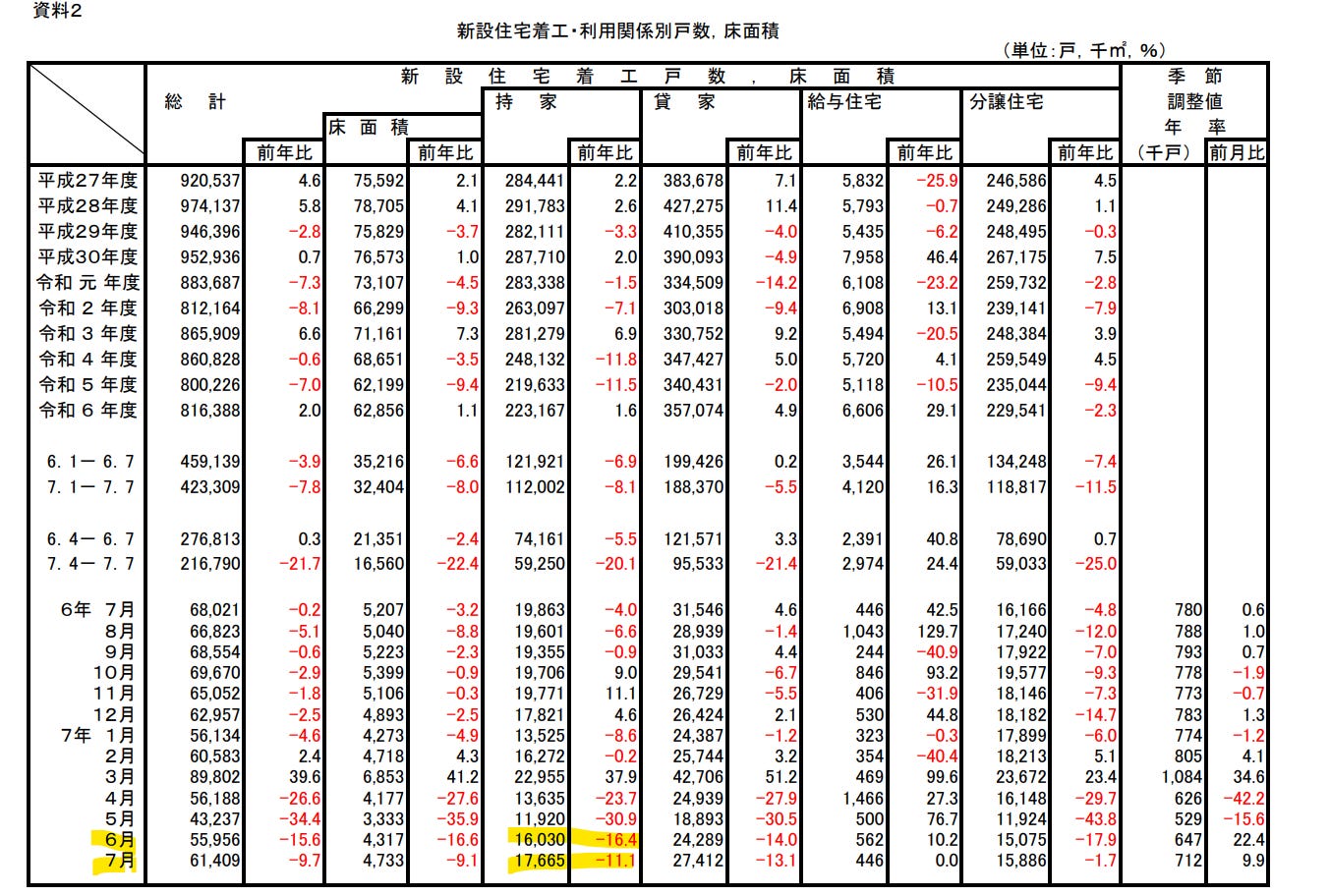

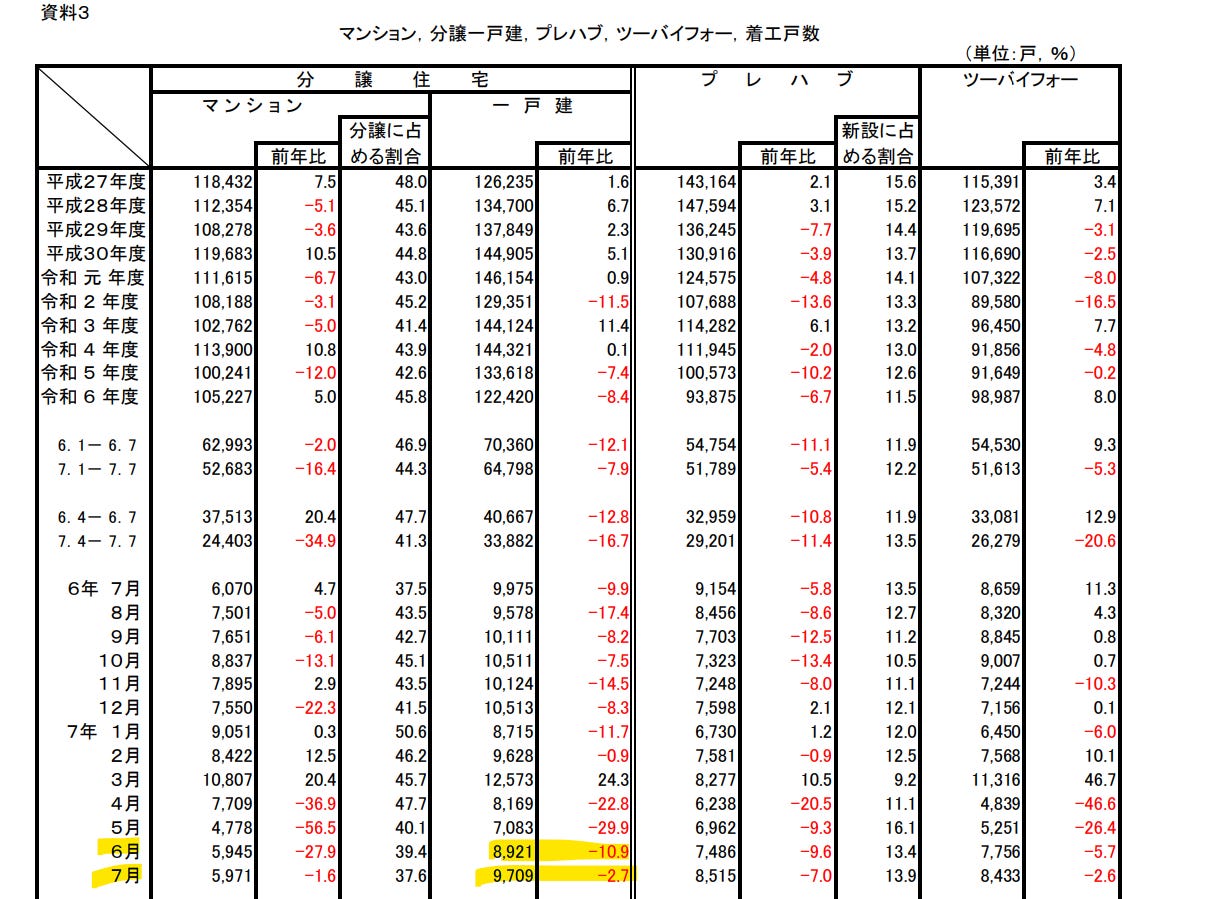

According to the latest government data, the housing start for a single family home recovers in June, July compared to May. Of course, the recovery is not strong, looking at the YoY is negative. However, the plunge is stabilized. It’s not so bad.(Link)

Based on demand/supply side situation, Noda has a plan for price revision. I hope it will improve the margin gradually.

Add one more thing for the amendment to the Building Standards Act from April 2025. The regulation for earthquake-resistant is stricter. So, Noda tries to promote the HBW(High Best Wood) product, which strengths the house structure.(Link)

Expanstion to rental, reform and non-residential fields

Looking at housing start statistics mentioned above, rental house market is relatively more stable than a single family house. Also, there is solid demand for reforming old house to attract a rental house customer. Generally, the wooden apartment is few compared with the reinforced concrete in Japan. However, considering the number of elderly living alone people will increase in aging Japan, its trend can be a tailwind for a wooden apartment. Warmth of the wood(*Elderly people spent almost time in wooden house since children), easy to get along with neighbors(*Wooden apartment is low-rise), low cost rent(*Wooden construction is cheaper than reinforced concrete. Pension is not enough, so they are more price sensitive than young people)

Also, Noda strengths in the non-residential field as well. They consolidate Aritomo kogyo(アリトモ工業) into financials from FY2025. This company provides a wood exterior construction service.(Link)

Thanks to these actions, the sales in FY2025 Q2 grew YoY. I think its strategy can get a new business opportunity to offset the weak demand for a single family house.

If the situation is improved, the current price shows PER is 5x

As I explained, the current difficulty mainly comes from cyclical perspective. There is a sign where business environment will be improved, considering demand/supply side change. If the profit move back to FY2023 level, the current price is PER 5x. Of course, there is uncertainty of recovery, when? However, I think the bad new has been already priced in.

Dividend 5% is enough for me, waiting for business recovery.

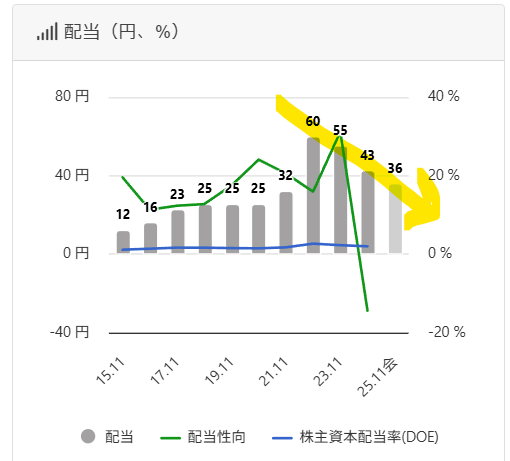

The proposed dividend is 36 yen for FY2025. Although dividend trend is downward recently based on the tough situation, it’s good to sustain at some level even if the net profit is negative(FY2024). In fact, the company says that they take care the divided stability in their dividend policy.

Considering FY2026 business performance can be better, thanks to the turnaround starts, the next year dividend can be increased. The current dividend yield is 5%. It’s enough for me. For dividend safety, Noda is Net-Net and net debt(=debt-cash) is negative(-9,940 million yen : cf. Noda market cap is 11,300 million yen). I think the annual dividend payment 563 million(*36 yen/share base) is not difficult for Noda.

Valuation

Net cash ratio = 1.02

Net cash ratio = (Current Asset + Investment Security * 0.7 - All liability - Non controlling interest) / Market cap

For the conservative valuation, I removed all ‘Non controlling interest’.

The current PER is 28x, but if the profit move back to FY2023 level, the current price is PER 5x.

Risk

The delay of price revision due to the demand side weak.

Missing the FY2025 guidance.

According to the latest FY2025 Q2 results, the progress toward guidance is not enough. The company tries to achieve the guidance by proposing to the rental, reform and non-residential market and raising price. However, they maybe miss. If so, the price will down more.

If you have enjoyed the post, please subscribe. Thanks for reading!

Thanks for the article. Interesting as always, but in this case it is too cyclical/turnaround for me :)